On Wednesday, February 26, the European Commission presented its adjustments to several key regulations related to reporting and sustainability. The goal is to simplify and revise several of its regulations under the Omnibus Directive, particularly by reducing administrative burdens and facilitating access to sustainable financing. But what exactly changes with this directive? Discover the key changes to come.

The goal of the OMNIBUS Directive

The European Green Deal (or Green Pact) is an ambitious roadmap adopted by the European Union to achieve carbon neutrality by 2050 and make the economy more sustainable. Omnibus regulations play a key role in its implementation by consolidating several directives and regulations that translate the Green Deal’s objectives into concrete obligations for businesses and member states. The Omnibus Directive* refers to a set of European regulations aimed at enhancing the transparency and sustainability of businesses. It includes several major texts, notably:

- The Corporate Sustainability Reporting Directive (CSRD): imposing increased transparency obligations on companies regarding their environmental, social, and governance (ESG) impacts.

- The Green Taxonomy Regulation: defining clear criteria to identify sustainable economic activities to guide investors and promote sustainable finance.

- The European Duty of Care (CS3D): introducing obligations for companies to identify, prevent, and mitigate the negative impacts of their activities on human rights and the environment within their value chains.

- The Carbon Border Adjustment Mechanism (CBAM): implementing a “carbon tax” for imported products into Europe, in certain industrial sectors (steel, iron, aluminum, cement, fertilizers, hydrogen, electricity…).

What is an omnibus law?

*An omnibus law is a law or legislative text that combines several measures or reforms into a single legal framework. It allows for changes to be made to different regulations at the same time, often with the goal of simplifying, harmonizing, or accelerating reforms.

What are the stated objectives?

One of the main objectives of the Omnibus Directive is to significantly reduce administrative burdens for EU businesses. The goal is to reduce overall administrative costs by 25% by 2025, and by 35% for SMEs, allowing for savings on annual administrative costs of approximately 6.3 billion euros.

SMEs, in particular, are expected to benefit from a substantial reduction in reporting obligations related to the Taxonomy, sustainability, and the Carbon Border Adjustment Mechanism (CBAM).

The Omnibus Directive also includes changes aimed at optimizing the use of European investment programs such as InvestEU. These changes will mobilize an additional 50 billion euros in public and private investments. The goal is to support priority policies such as competitiveness, energy transition, and environmental sustainability. By simplifying administrative requirements and increasing investment capacity, the EU hopes to stimulate innovation and sustainable growth.

CSRD

The CSRD aims to strengthen and standardize corporate sustainability reporting requirements in order to align the information provided by companies with the EU’s climate and environmental goals.

Key changes for the CSRD:

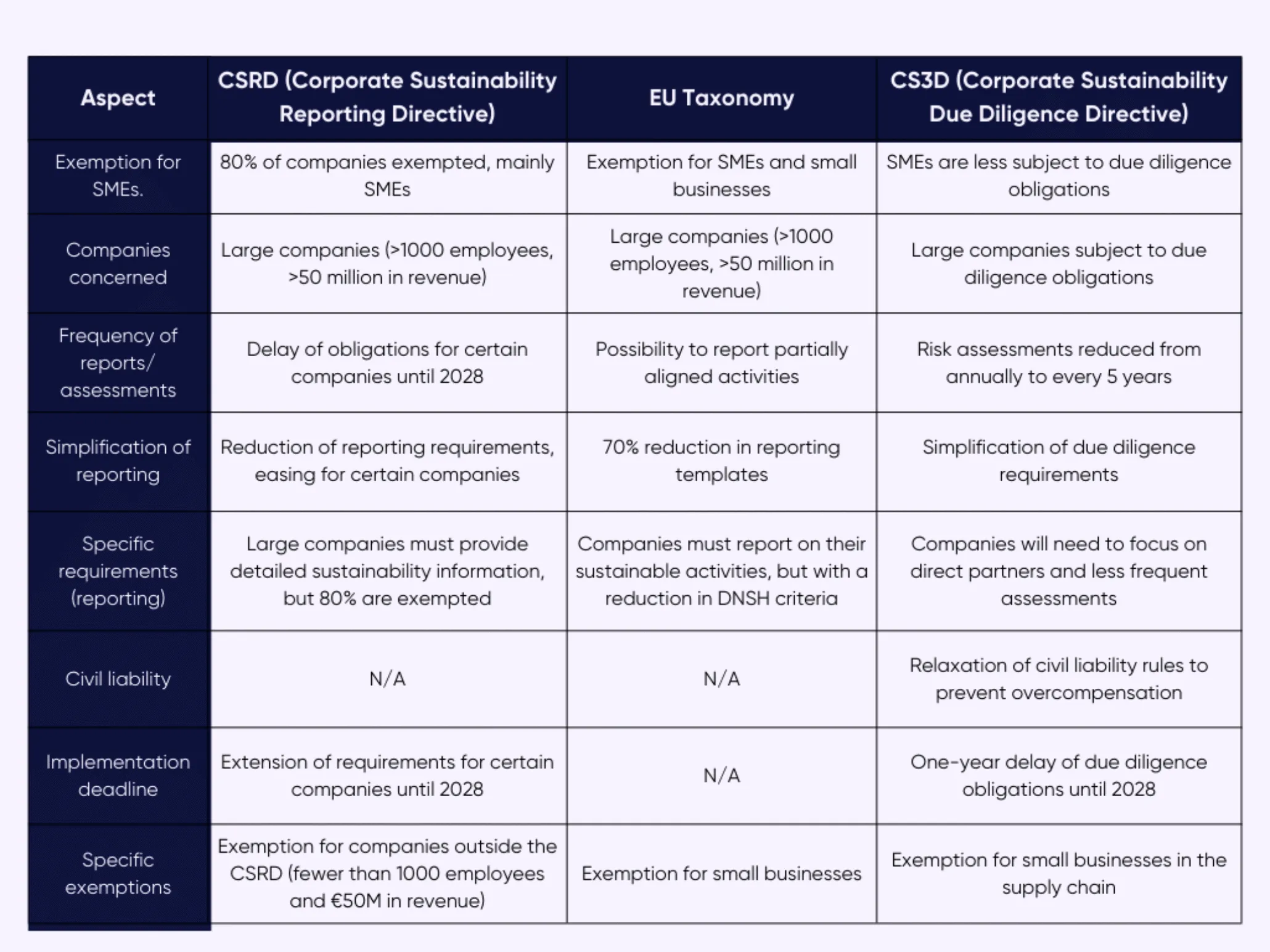

Exemption for small businesses: The Omnibus Directive will exempt about 80% of companies from the obligation to comply with the CSRD requirements, primarily small and medium-sized enterprises (SMEs). Only large companies, defined by a threshold of 1,000 employees and 50 million euros in revenue, will continue to be subject to these detailed sustainability reporting requirements.

Reduction of requirements for large companies: Reporting will be simplified for certain large companies, reducing the number of criteria to report, and making sustainability obligations more targeted, particularly focusing on significant environmental impacts.

Delay in reporting requirements for certain companies: Companies currently subject to the CSRD, which were supposed to start reporting from 2026 or 2027, will see their obligations delayed by two years until 2028. This will give them more time to adapt.

CS3D

The CS3D aims to hold European companies accountable for due diligence and sustainability. It imposes obligations on companies to identify, prevent, and mitigate environmental and social risks throughout their supply chains.

Key changes for the CS3D:

Simplification of due diligence requirements: Due diligence obligations will be simplified, particularly for companies with direct business partners. This reduces administrative complexity, especially for companies with vast and complex supply chains.

Reduction in the frequency of assessments: Companies will be required to conduct periodic environmental and social risk assessments within their supply chains, but the frequency of these assessments will be reduced from annually to every 5 years. The aim is to reduce the workload for companies while maintaining regular risk monitoring.

Simplification of information requested for SMEs: Large companies will no longer request as much information from SMEs within their supply chains. As a result, SMEs will have less documentation to produce, reducing their administrative burden.

Increased harmonization of due diligence requirements: Due diligence requirements will be better harmonized across the EU to ensure a level playing field for all European companies, reducing national disparities and additional administrative burdens.

Relaxation of civil liability rules: Civil liability conditions will be adjusted to protect companies from overcompensation in case of non-compliance, while ensuring that victims of violations receive full compensation.

Delay in implementation deadlines: The deadline for large companies to comply with the CS3D directive will be extended by one year, until July 2028. This will give companies more time to prepare for the implementation of the new rules.

Taxonomy

The EU Taxonomy is a classification system that determines whether an economic activity is environmentally sustainable. It plays a crucial role in redirecting investments towards activities that support the ecological transition.

Key changes for the EU Taxonomy:

Limitation of reporting to one category of companies: Only large companies will be subject to reporting obligations under the EU Taxonomy. SMEs and small-medium enterprises will be exempt from these complex obligations, thereby reducing the administrative burden.

Ability to report on partially aligned activities: Companies will now be able to report activities that are partially aligned with the Taxonomy, allowing for a more gradual transition to a sustainable economy. This encourages companies to take steps to progressively reduce their environmental impact, rather than waiting for full compliance.

Reduction of “Do No Significant Harm” (DNSH) criteria: The “Do No Significant Harm” (DNSH) criteria, which prevent companies from harming the environment in their processes, will be simplified. This particularly concerns pollution prevention and chemical use, making compliance easier for companies while ensuring environmental protection.

Exclusion of small businesses from Taxonomy reporting obligations: Small businesses will be exempt from detailed financial and environmental reporting under the Taxonomy, unless they choose to voluntarily report their sustainable activities.

Reduction in reporting templates: Reporting templates will be reduced by 70%, further simplifying the process for businesses.

Next steps

The legislative proposals of the Omnibus Directive must now be reviewed by the European Parliament and the European Council for adoption. If the proposals are validated, the changes will come into effect in 2025. Therefore, companies must prepare for these reforms, particularly by adjusting their reporting and due diligence practices. The goal is to ensure a smooth transition to the new standards, while continuing to promote a green and competitive economy.

Limare Charlotte

Share